How do you use a yellow financial pad for your budget?

When I started actively planning our budgets, I wanted something that wasn’t necessarily on the computer, something I could physically stick under my husband’s nose and get him to look at and review. Some people recommend a legal pad, but I'm an Excel junkie and I like things to line up. I liked the order that came with yellow accounting pads, with all those perfect little lines and columns. When you're dealing with money, accuracy counts!

The trouble was that I had no idea where to start if I was going to use a financial pad for personal use. It took me a while to find a visual example, and it was one really grainy online photo that I zoomed in far enough to puzzle it out - kind of. The rest I learned as we went, month-to-month, perfecting the process and layout.

A quick tutorial on how to use a yellow columnar sheet.

I’ve played around a little and adapted this for our use, and what works best for my brain. After a few months with this, you may find you want to do that too. There’s no right or wrong way to do this - it's not like you've got a job or a grade riding on “perfect” use. Perfect is the enemy of good. I've plugged in some sample numbers to show you how this works.

1. Note the month and label your columns.

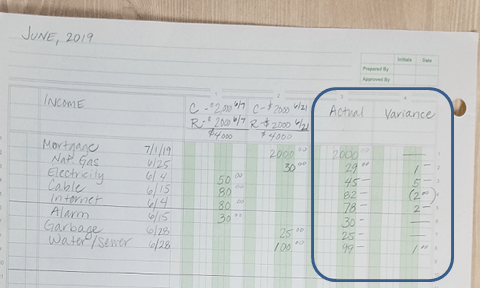

Let’s lay the foundation of your monthly budget with some categories and basic information. Note the month up in the corner, and then in header area of the widest column, write “Income.” In columns 1 and 2, you’re going to note your paychecks. Before you get all excited and write stuff down and then have to erase later (Did I remind you to do this in pencil? No? Remember to use pencil!), let me explain the other columns - column 3 will be for "Actual" expenses, and column 4 will be your "Variance," to see how your actual differed from your plan.

In the income columns, I write either our initials, or full names if I’m feeling saucy. I also note the dates that those dollars are expected to come in. As I mentioned above, I’m using some representative figures here, but I wanted to show what this really looks like.

2. Plug in your income.

Note – your paydays may or may not line up together. Ours don’t. Sometimes I group them together so that they line up by one of the dates. My husband gets more deposits in a month than I do, so I just figure that by the date that my first one comes in, he will have deposits 1 and 2 in the account. I add them together and write the total of those two deposits on his line, with the same date. For example, $1,000 deposited on the 7th and $1,000 deposited on the 14th would be combined into $2,000 by June 15, coinciding with the mid-month check of the other person. We only have so many columns, and this makes it simpler as we go. Note that I use one line for me, one for him, and the bottom line in this box for the combined total.

3. Group and list your expenses.

Next, go down the wide, left-hand column and note your expenses. The little sections on these yellow sheets make it easier to group them together into categories, though you might have some spill over if you have more than five items in a group. You’re going to have one line for each biller or item.

Housing is your most important expense category, so put that down first. That’s your mortgage or rent payment, and any separate bills you have that are related to your housing – HOA dues, etc. My next category is utilities– water and garbage, electricity, natural gas, TV, etc. The next group is food (groceries, eating out and school lunch), followed by transportation (gas and oil, parking, insurance and tolls), lifestyle & entertainment (haircuts, pet costs, gifts, clothes, gym) and lastly, debt. Don’t forget your autopay items!

and note the date the bill is due

4. List the bill amounts under the appropriate paycheck column.

When I budget for the upcoming month, it's rare that I have all my bills in hand. I recommend looking at what you paid last month for each item, to get an approximate amount for the upcoming bill. List each amount due in the column under the paycheck(s) that will pay that bill. For example, a Visa bill due on the 24th of the month will go into the June 15th paychecks column, but a water bill due on the 8th will need to be paid for with funds that are in your account on the 1st of the month (or somewhere thereabouts). That way you know you have the funds in your account when the bill needs to be paid.

How do I budget for bills due before the first paycheck?

Sometimes it’s hard to think about an item being paid on the first of the month, when you may not get your first paycheck of that month until the 7th, or some other day that isn’t the exact FIRST. For those, I recommend playing a bit of a mind game, and figuring in “next month’s” payment. So as I budget for June, I’m planning on July’s mortgage payment that gets paid monthly on the first, because I’ll need to have money in hand before that bill is due. In the image above, you'll notice I put the mortgage payment for July 1 in the later "paycheck" column. Make sense?

5. Total your expense columns and subtract.

Once you’ve listed everything, add up each column's expenses, and subtract the total from the combined income up at the top of that column. As your month goes on, go back in at least once a week and fill in Column 3 with whatever the ACTUAL costs/bill amounts were for the item in each row. In column 4, note the difference between what you budgeted and what the actual amount spent was – did you come in under and have money left over, or did you go over budget?

the difference from what you budgeted.

Assess and adjust, if necessary.

That "Variance" column is there to help you recognize overspending and help you perfect your month-to-month budgeting. Knowing the reality of your monthly bills will help you get better next month, and even better the month after!

There you have it! A step-by-step tutorial on how to do a personal budget with a yellow columnar pad. Go forth and budget!